Canada’s Prime Rate in 2023: All You Need to Know{2024}

Explore the information on Canada’s Prime Rate for 2023 in this article. It covers all the essential details about the Prime rate in Canada.

Prime Rate Canada 2023

The Prime Rate serves as the interest rate employed by banks, typically reflecting the rate at which they offer loans and mortgages. In Canada, the Prime Rate is commonly influenced by the Bank of Canada’s policy interest rate, known as the BoC’s overnight rate. Following adjustments to the overnight rate by the BoC, other lenders tend to align their prime rates accordingly. This rate is frequently utilized as a reference point for determining adjustments in rates for things like adjustable-rate mortgages and other short-term variable-rate loans.

Canada Prime Rate Overview

| Name | Prime Rate |

| Also known as | Prime Lending Rate |

| Country | Canada |

| Influenced by | Target for the overnight rate |

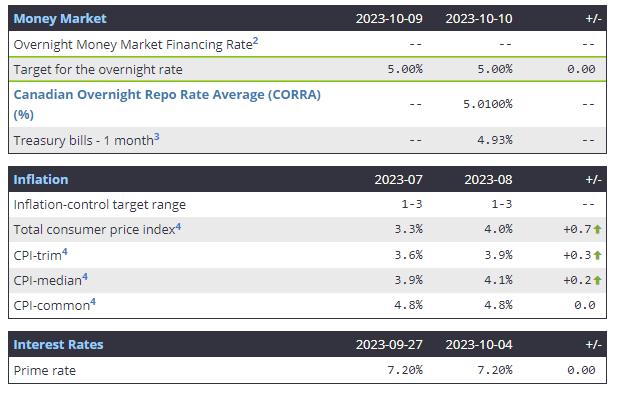

| Prime Rate in Canada | 7.20% |

| For more information | https://www.bankofcanada.ca/rates/daily-digest/ |

What is the Prime rate in Canada?

The current Prime Rate in Canada stands at 7.20%. It holds significant attention as it directly impacts variable interest rates. Major banks typically align their Prime Rates, and it consistently tends to be higher than the Policy Interest rates.

Over the years, the Prime Rate in Canada has experienced notable fluctuations. On June 7, 2023, it was recorded at 6.95%, undergoing a 0.25% increase within a few months to reach 7.20%. Detailed information, including various rates, statistics, and supporting data, can be accessed on the official website of the Bank of Canada.

Additionally, the website’s daily digest section offers insights into inflation, exchange rates, interest rates, money markets, and bond yields. As per the Bank of Canada’s daily digest, the Target for the overnight rate is 5%, CORRA stands at 5.0100%, and the Real return bond – Long-term is 2%.

How Prime Rate Impact the Interest Rates?

As previously stated, the Prime Rate directly impacts the interest rates set by lenders for loans and various financial products.

Lines of Credit:

A Line of Credit is a credit facility that provides customers with the flexibility to access funds when needed. For unsecured lines of credit, the interest customers pay on their balance can change without prior notice if there are fluctuations in the prime rate. In the case of secured lines, like a Home Equity Line of Credit (HELOC), an increase in the prime rate can result in higher interest rates on the outstanding balance.

Credit Cards:

While most credit cards have fixed interest rates, some are linked to changes in the Prime rate. This means that if the Prime rate rises, the monthly interest payments on outstanding balances will also increase. Customers utilizing such credit cards should remain vigilant about changes in Prime Rates.

Variable-rate Loans:

Interest rates on variable-rate loans are often tied to the Prime Rate. Borrowers need to monitor the Prime Rate as it determines the manageability of their loan payments. Generally, an increase in the Prime Rate doesn’t directly raise monthly payment amounts, but some portions may shift towards interest rather than principal, potentially extending the repayment period.

All We Know About Prime Rate in Canada

The Prime Rate in Canada has the potential to undergo eight adjustments in a given year. In 2022, the prime rate changed six times following announcements from the Bank of Canada (BoC). Subsequent alterations will be contingent on the decisions regarding the BoC’s policy interest rate. Historical data indicates that the Prime Rate peaked at its highest percentage in 1981, reaching 22.75%, and hit its lowest percentage in 2009, registering at 2.25%.

Therefore, when the prime rate decreases, the interest on loans linked to the Prime Rate also decreases. This results in a higher portion of payments being allocated towards the principal amount. Reduced interest rates can lower the overall costs of borrowing, often prompting increased spending by individuals. This, in turn, contributes to an economic boost for the country.